The Journey

THE CHALLENGE

A large retail bank was looking at automating their Regulatory Credit Risk Reporting requirements.

THE SOLUTION

The Bank has been using the ElysianNxt IFRS 9 platform which already hosts their internal models for PD, LGD and EAD models. This provided an ideal starting point for credit risk regulatory reporting.

THE OUTCOME

Following the success of the IFRS 9 project, the bank decided to extend the use of the platform further and have implemented Basel III and Basel IV, respectively.

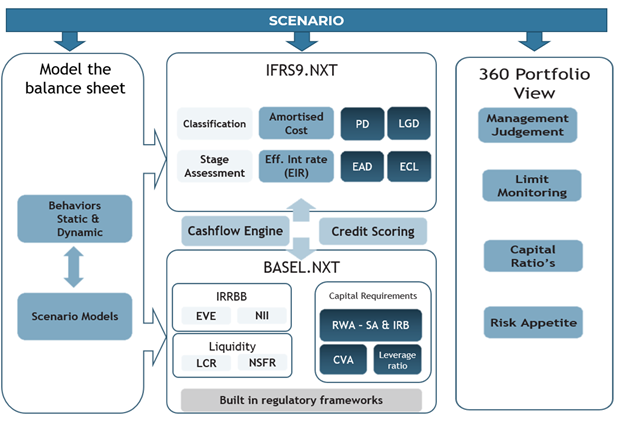

The Bank now has all its credit risk data centralized into the ElysianNxt platform. The universe of data, combined with the platform’s performance and user-friendly interface enables the bank to strive for the optimum end-state; a fully integrated stress testing framework.

- The regulator decided to take lessons learnt from other countries in the region before enforcing the rules on their banking industry, thus delaying the adoption date of IFRS 9 to 2020 with a 6 month parallel run starting July 2019.

- The Bank witnessed how other large financial institutions in the world struggled with IFRS 9, specifically on performance, as most solutions in the market were ill-equipped to handle IFRS 9’s complex calculations for large volumes of data.

- The Bank then went looking for a high-speed, performant IFRS 9 solution that could accommodate their massive data volumes. They invited ElysianNxt, along with other large names in the industry, to participate in a proof of concept (POC) to prove the solution’s capability to run 9 million contracts in less than 5 hours.

- ElysianNxt’s solution came out on top – the solutions’ streaming architecture and advanced technology met and exceeded the POC objectives.

- In the 6 months leading to the January go-live date, they ran at least 30 ECL calculations to fine-tune their models, methods and data.

- In June 2019, the bank went live with ElysianNxt’s IFRS9.NXT – on budget and 6-months ahead of deadline.

- The Bank’s internal models for PD, LGD, and EAD were originally hosted outside of ElysianNxt. This caused processing delays as the former processes’ calculation speed was too slow to meet EOM requirements. The former process also lacked a User Interface that would empower users to maintain or change models.

- The Bank decided to onboard their models into ElysianNxt. Vastly improving control, transparency and performance.

- The Bank decided to extend the use of the platform further and greenlit the implementation of Basel Ill in September 2020, replacing their current system. In only three months the bank successfully migrated to the ElysianNxt Basel solution.

- The Bank then decided to keep the momentum going and embarked on implementing Basel IV two years ahead of the regulatory deadlines. This made them one of the first banks globally to be live with Basel IV, and they did so in only two months.

THE JOURNEY CONTINUES...

- The Bank now has all its credit risk data centralized within the ElysianNXT platform.

- The universe of data, combined with the platform’s performance and easy-to-use interface, enables the bank to strive for the optimum end-state; a fully integrated stress testing framework.

- Full bottom-up stress tests in minutes rather than hours.

- Centrally defined stress scenarios that can be attached to every calculation.

- The head of risk reads the newspaper and gets alarmed by the news of a new Covid variant that could put the world economy back in a 6-month lockdown.

- They ask one of their risk analysts what the impact would be on the key risk metrics. The analysts logs into the ElysianNxt platform, defines the worst-case stress scenario, and runs it through all credit risk metrics.

- Before lunchtime, a detailed impact analysis across all the banks’ key risk metrics can be presented.

The ElysianNxt stress testing framework offers the bank a complete 360° view on the results of the stress test. The integrated and purpose-built dashboards display the impact of the stress scenario on all risk metrics.

The ElysianNxt stress testing framework offers the bank a complete 360° view on the results of the stress test. The integrated and purpose-built dashboards display the impact of the stress scenario on all risk metrics.

– Piet Mandeville, Product Director, Risk – ElysianNxt